The auto market didn’t get harder

It got structurally different

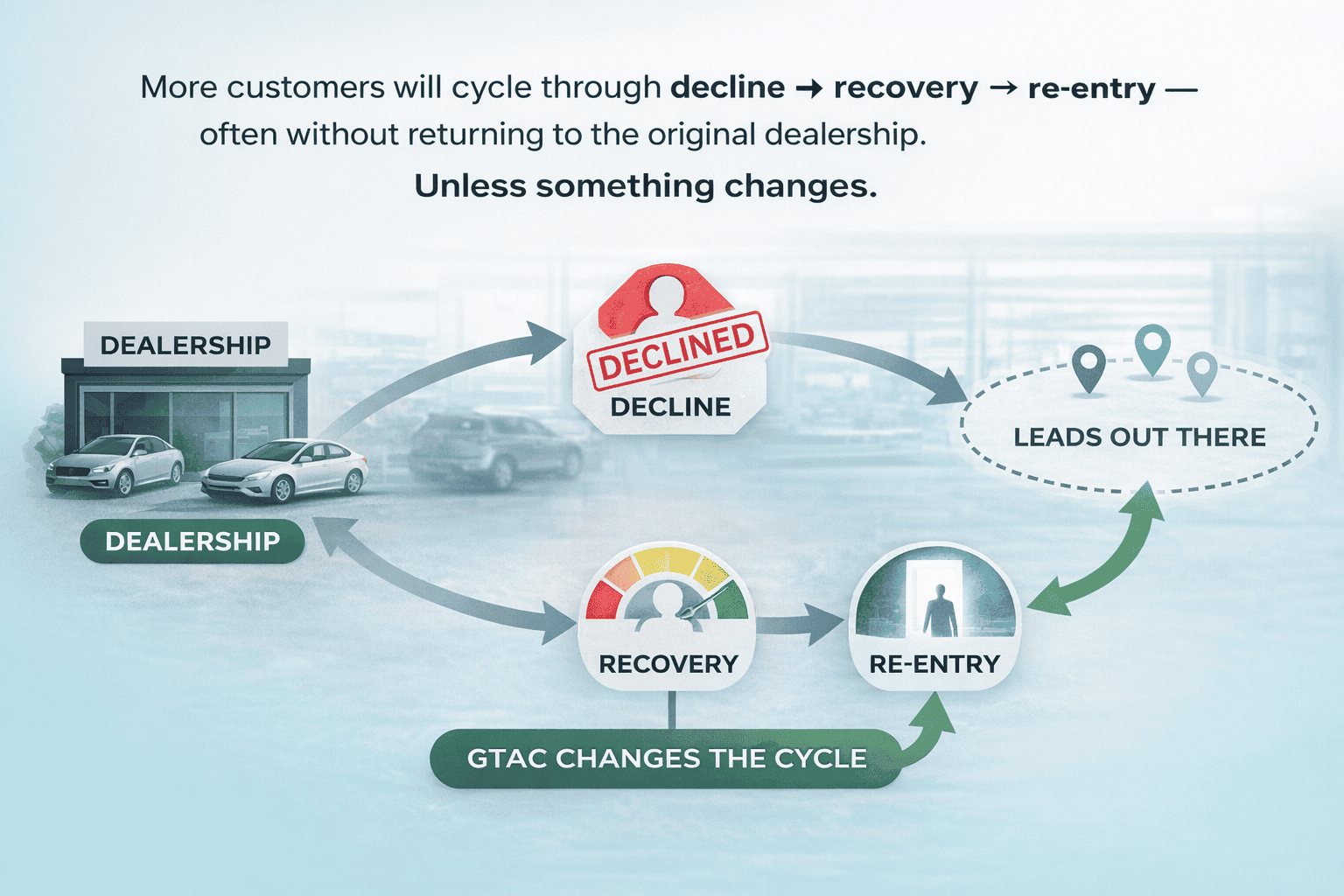

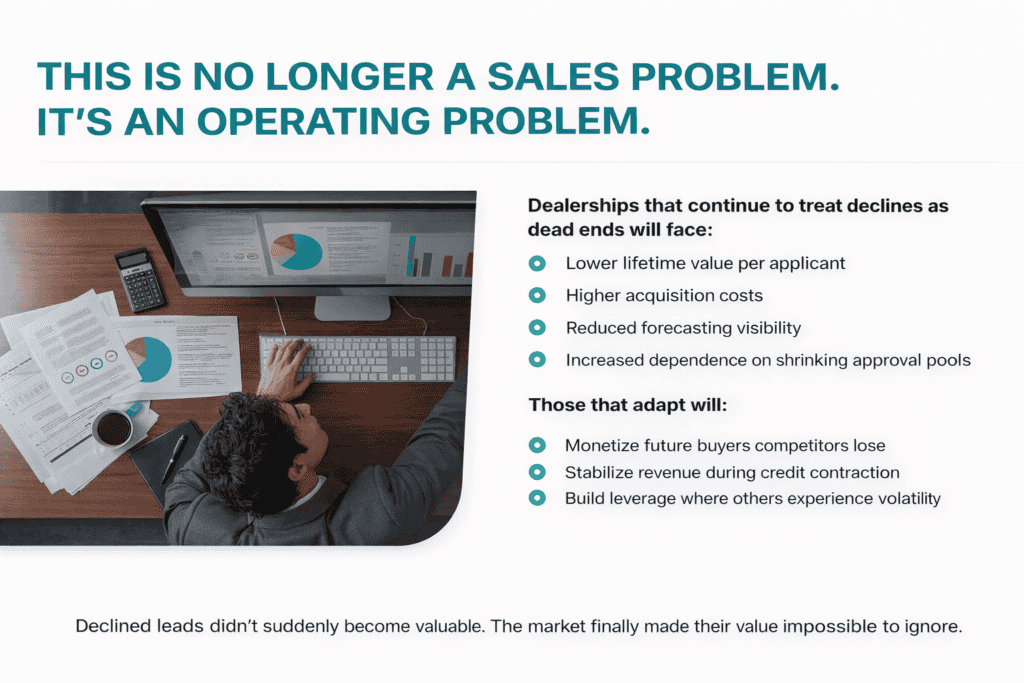

The rules that governed approvals, lending, and buyer behavior for decades no longer apply. Dealerships that don’t adapt their post-decline strategy will quietly lose market share in the years ahead.

CREDIT CONTRACTION IS NO LONGER THEORETICAL

For years, auto retail benefited from abundant and flexible credit. That environment has shifted:

Tighter underwriting standards

Reduced subprime and near-prime approvals.

Lenders exiting the market or dramatically scaling back

Increased scrutiny on risk exposure

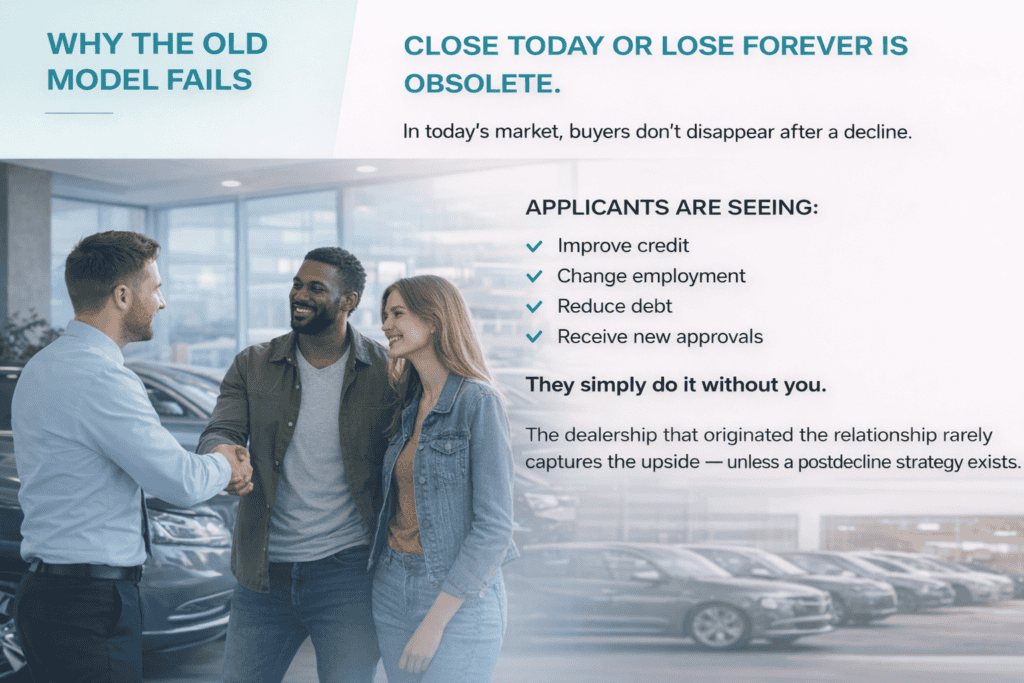

The result is not fewer buyers it’s more temporarily unfinanceable buyers.

Customers aren’t gone. They’re delayed.

WHEN LENDERS STRUGGLE, DEALERSHIPS ABSORB THE IMPACT

As lending institutions restructure, consolidate, or fail, the effects are felt first on the showroom floor.

Dealerships are seeing:

Sudden guideline changes

Inconsistent approval

Reduced flexibility for borderline applicants

Higher fallout rates after submission

Declines are no longer edges cases.

They are becoming a structural feature of the market.

Risk is being pushed backward — onto dealerships

Rising auto loan delinquencies and repossessions are forcing lenders to protect themselves.

That protection shows up as:

Narrower approval windows

Higher scrutiny on credit profiles

More conditional approvals

Faster decline decisions

This doesn’t eliminate demand.

It compresses timing.

Declines now outpace dealer follow-up capability

Sales teams are built to close deals, not to manage delayed buyers over months or years.

CRMs weren’t designed to:

Educate declined applicants

Monitor readiness over time

Re-engage buyers when conditions improve

Capture downstream value

So declined leads fall into a blind spot.

Not because dealerships don’t care

but because the system was never built for this environment.